5 Bank Fees You Should Never Pay Again

5 Bank Fees You Should Never Pay Again

April 04, 2018

- Banks make billions of dollars by charging customers fees

- Common fees include for ATM usage, paper statements, or overdrawing accounts

- Fact: You can avoid or minimize most bank fees

No matter how you slice it, nobody likes bank fees.

We’ve all been there—when you take a look at our bank statement or account balance, only to find that you have less money than you thought. Where did it go?

Then you see it: Your bank has hit you with fees that you never anticipated. It could be for simply accessing your money, having too low a balance, or even receiving your paper bank statement. It’s enough to make you want to keep your money in your mattress.

A dollar here, $20 there—these bank fees can really add up. In 2016, for example, consumers were charged $34 billion in overdraft fees—and that’s just one of many kinds of fees many banks charge.

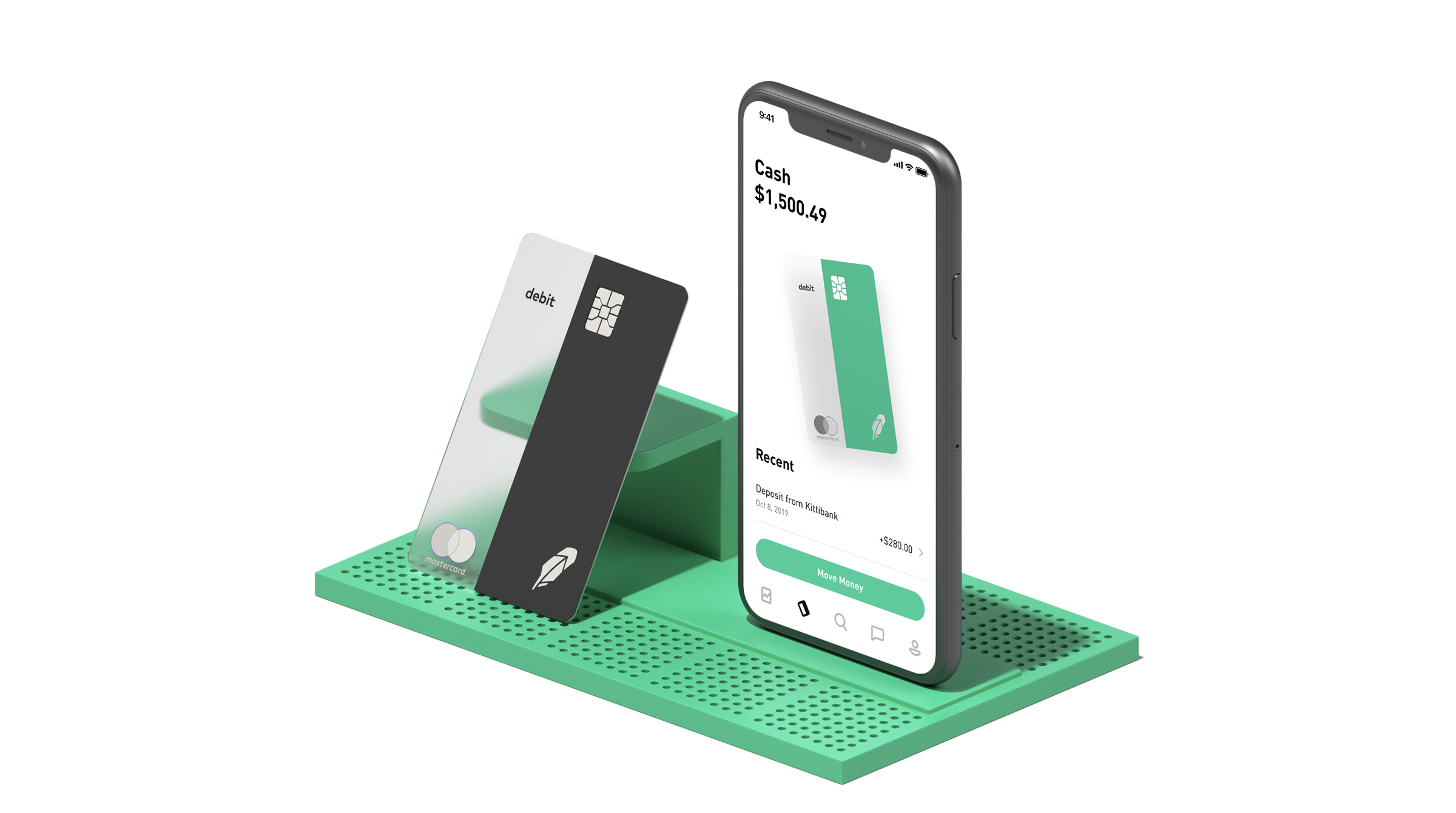

Note: Stash debit can help you avoid excessive bank fees. It won’t cost you anything to set up, there are no minimum balance requirements, and we won’t charge you any monthly or annual fees to maintain the account1.

Here are five of the most common fees banks like to charge, and ways to avoid them.

1. ATM fees

- What it is: A fee for withdrawing money from an ATM machine.

- Average fee: $4.69, according to recent industry data

How to avoid it: Banks typically charge ATM fees when you’re withdrawing money from an out-of-network machine—or, an ATM that’s owned or operated by another institution.

To avoid ATM fees, get cash from your own bank’s machines, or go inside and do it the old-fashioned way: Speak with a teller. (Just make sure your bank doesn’t charge a teller fee, see below.) You can also get cash back when you make a purchase with your debit card to get cash or switch to a bank that refunds ATM fees.

You can also shop around for a bank that covers a certain number of out-of-network ATM fees.

The Stash debit card gives you access to thousands of fee-free ATMs around the U.S.2 You can deposit cash to your account through your linked bank account, via direct deposit, or at participating CVS Phamacy®, Rite Aid and Walgreen stores3.

2. Account maintenance fees

- What it is: A fee levied to service your account, typically your checking account. Maintenance fees are sometimes called minimum-balance fees.

- Average fee: Variable (Bank of America and Chase, for example, charges $12 per statement cycle for balances under $1,500; Wells Fargo charges $10.

How to avoid it: If your bank charges custodial and maintenance fees, ask if they have a different kind of checking account option that doesn’t have minimum balance fees. If not, the easiest way to dodge them is to switch to a bank that doesn’t charge them in the first place. Otherwise, you’ll need to abide by your bank’s rules in regard to balances and deposits.

As a last-ditch effort, you can try arguing with your bank to get these charges refunded. The customer service agent may be kind and refund a month or two to keep your business—but that probably isn’t going to prove a fruitful long-term strategy.

3. Overdraft, and/or non-sufficient fund (NSF) fees

- What it is: A charge for overdrawing your account, and for the bank covering the difference.

- Average fee: Around $35

How to avoid it: One of the biggest money-makers for banks, overdraft fees are also the hardest to swallow. If you overdraw your account, you’re basically borrowing money from your bank—and your bank is happy to lend it to you at an incredible markup.

The difference between an NSF and overdraft fee is small but important. When you’re charged an overdraft fee, the bank covers the charge for you. When you’re charged an NSF fee, the transaction isn’t approved, as the bank declines to pay it on your behalf. You’ll be charged one or the other, depending on which action your bank takes.

If you write a check for more than your account balance, it’s possible that you’ll be hit with an NSF fee or overdraft fee, and the recipient will also be levied a returned-check fee. This is a fee charged by the recipient’s bank for depositing a bounced check.

One way to think about it is if you borrowed $24 and were hit with a $34 overdraft fee, you’d be paying 17,000% APR, according to the Consumer Financial Protection Bureau.

How can you dodge these fees? You’re entitled to decline or cancel overdraft coverage. If you cancel the coverage, the transaction will be declined, saving you from overdrawing.

A word of caution: Always, be aware of your account balances and plan purchases accordingly.

4. Paper statement fees

- What it is: A fee incurred for receiving a paper statement from your financial institution

- Average fee: Varies, but usually around $1

How to avoid it: It’s simple: Sign up for electronic statements, delivered via email. This is as easy as it gets, and while it may only save you a buck or two a month, it’s another dollar that can go toward your investment portfolio or retirement savings. Electronic statements are also good for the environment because they don’t require paper.

5. Teller fees

- What it is: A charge for talking to a live person—be it a teller or another bank representative

- Average fee: $3-$5, depending on account type

How to avoid it: Teller fees aren’t new, and the concept has been around since at least the mid-90s. They’re generally associated with online-only accounts, which typically don’t include in-branch services.

If you think you’ll need more than attention than an online-only account provides, opt for a traditional checking or savings account to avoid teller fees. Eighty-four percent of bank customers still visit their bank in-person, so be mindful of these teller fees if you do sign up for an online-only account.

In : 848FINACE

Tags: bank fees banking saving accout jp morgan citi bank chase bank